The Philippine economy is expected to grow 7 to 9 percent in 2022, one of the highest in Asean. This upbeat scenario is due to our moderately successful vaccination efforts and low COVID-19 cases, which merited the downgrading of NCR and many parts of the country to Alert Level 1.

According to the National Economic and Development Authority, if the entire country is at Alert Level 1, the lessened mobility restrictions will result in a weekly economic activity increase of P16.5 billion, domestic tourism rebound of P750 billion in 2022, and 297,000 new jobs in the second quarter alone—all of which underscore the importance of every Filipino observing minimum public safety protocols.

It is to our best interest to avoid another COVID-19 surge, which is currently being experienced by other Asian countries with much higher vaccination rates than ours.

‘Back-to-office’ mandate

One of the hottest business topics currently is the Department of Finance’s (DOF) back-to-office mandate to the business process outsourcing (BPO) industry by April 1, wherein non-compliance will result in losing some tax perks.

The industry is seeking a phased approach that will span six months but the DOF seems to be adamant with its order. The real estate industry is watching the next actions on this as it will significantly impact the office, retail and the residential segments of the industry.

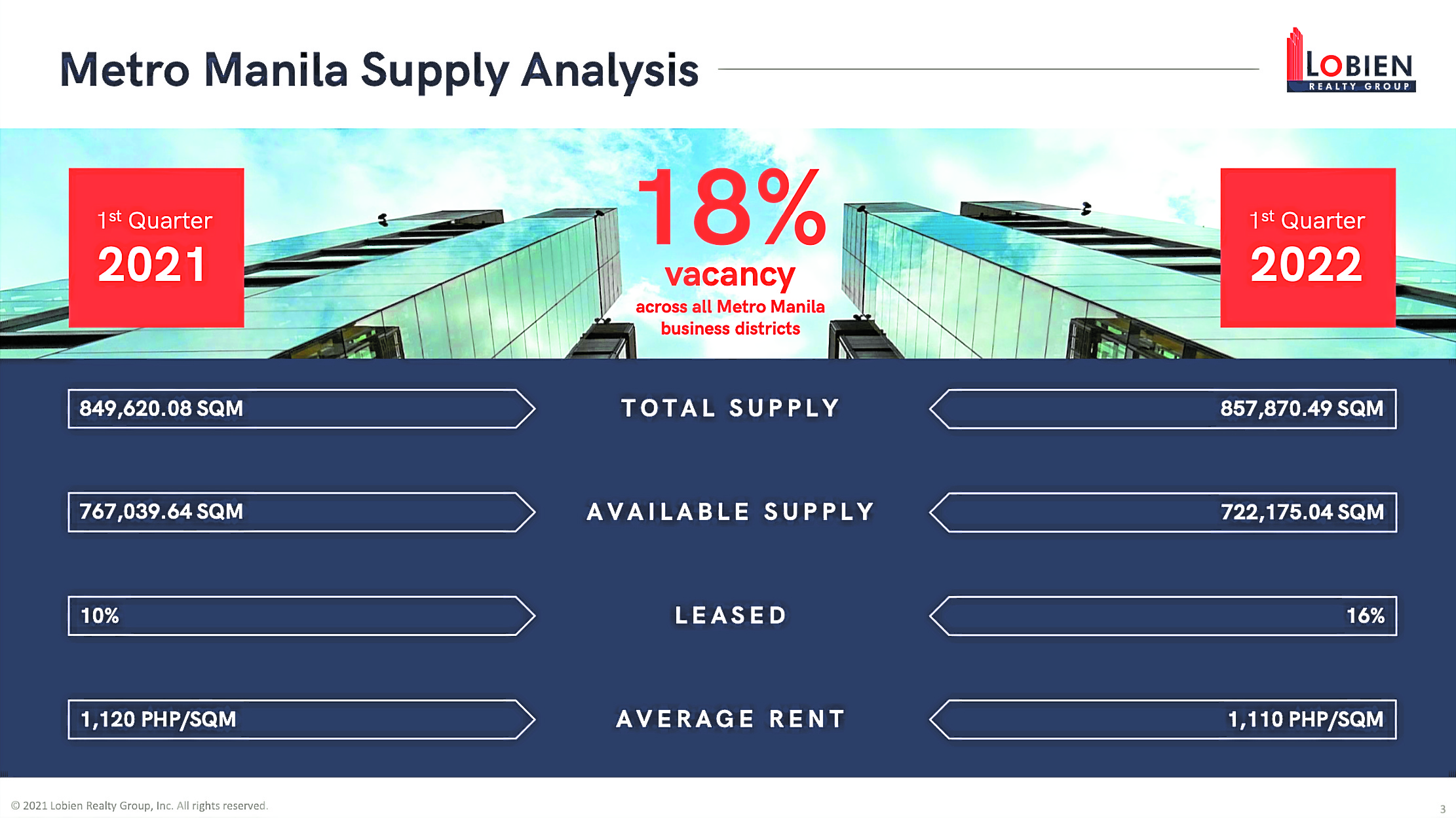

As of end 2021, the office space industry has a vacancy rate of around 13 percent, which translates to unoccupied office space totaling 1.6 million sqm.

The BPOs’ return to office will result in a take-up of around 450,000 sqm in NCR alone, based on the estimated 180,000 new jobs created by the industry in Metro Manila for the years 2021 to 2022. The government may need to balance the advantages of the WFH set-up for the BPO industry with the economic rationale of the back-to-office order.

Improved competitiveness

The signing of Republic Act No. 11659, which amends the Public Service Act, is a welcome news to the business community—and may prove to be very significant in the country’s economic recovery and long-term competitiveness.

As of 2020, the Organization for Economic Cooperation and Development (OECD) ranked the Philippines as the third most restrictive economy globally.

Allowing foreign ownership up to 100 percent in telecoms, railways, subways, expressways, tollways and airlines is expected not just to address the restrictiveness ranking but more importantly, to spur foreign direct investment and economic growth and address the poor infrastructure situation of the Philippines.

IMD’s 2021 World Competitiveness Report ranked the Philippines 59th out of 62 countries—a dismal performance even in light of the current administration’s massive Build, Build, Build spending for the past five years.

Elections

Meanwhile, we are less than 50 days to the elections and the results will definitely have an impact on how the country will be run for the next six years.

It is everyone’s hope that our decision will serve us well as a nation and may it start with a resounding economic recovery this year.

Sheila Lobien is the chief executive officer of the Lobien Realty Group.

By Sheila Lobien