Lobien Realty Group is the No. 1 Realty Property Provider in the Philippines. We provide office and commercial spaces, lots and properties for sale/lease in the cities of Makati, Taguig, Pasig, Mandaluyong, San Juan, Pasay, Parañaque, Las Piñas, Quezon, and Caloocan.

July 15, 2025

Lobien’s 2025 mid-year report of the real estate industry

NCR and provincial office market vacancy high, warehousing sector growing

Vacancy rates remain high in the office sectors in both the National Capital Region and the provinces. The residential condominium market in Metro Manila is currently “a buyer’s market”. Meanwhile, warehousing industry in the country is robust and continues to grow. These were the highlights of the 2025 mid-year report on the real-estate industry presented by leading real estate property provider Lobien Realty Group, Inc (LRG). on July 9.

The current Philippine economy

First, the LRG team gave as context the current state of the Philippine economy which grew 5.6 percent in 2024, the second fastest GDP growth among ASEAN countries last year. This growth momentum is expected to continue in the next two years as the Asian Development Bank (ADB) projects a GDP growth of 6 percent in 2025 and 6.1 percent in 2026 for the country, underpinned by strong domestic demand, continued investments and stable inflation rate.

As of Q1 2025, the economy grew 5.4 percent year-on-year (y-o-y) with all major sectors registering growth, led by services at 6.3 percent, industry at 4.5 percent, and agriculture at 2.2 percent. Household final consumption expenditure expanded 5.3 percent while total investments grew 4 percent y-o-y. Inflation also slowed further to 2.2 percent, which is well within the government’s 2 to 4 percent target band; this gave ample support for the 50-bps year-to-date reduction in policy interest rate, which stood at 5.25 percent as of June 2025 coming from 5.75 percent at the start of the year. Further reductions in policy interest rate will benefit the real estate industry in its recovery efforts.

The office market in Metro Manila

New office supply, existence of vacant office spaces left by the Philippine Offshore Gaming Operators (POGOs), and y-o-y contraction in lease rates (from 42 percent in Q2 2024 to 14 percent in Q2 2025) pushed vacancy rate to 20 percent and rental rates to decrease to Php 950/sqm. This challenging situation for the office space sector is primarily due to slowdown in global growth, geopolitical conflicts in Asia and in the Middle East, and the country’s relatively high policy interest rate when compared to historical averages. This is how LRG CEO Sheila Lobien assessed the office market in Metro Manila.

For the period 2009 to 2019, Philippine GDP growth averaged 5.957 percent while policy interest rate averaged 3.775 percent, while the last 5 years’ average for GDP has been 2.998 percent and 4.35 percent for policy interest rate. For the same period, we also saw a sequential annual increase in rental rates, which doubled from Php 503/sqm in 2009 to Php 1,160/sqm in 2019 and vacancy rate being stable at 5.5 percent.

On the supply side, the same GDP and interest rate scenarios also resulted in sequential annual increases in office supply, with the annual supply of 600,000 sqm in 2009 almost doubling to 1,800,000 sqm in 2019. During this period, annual office supply delivered to the market averaged 855,000 sqm while only 500,000 sqm were constructed on a yearly basis for the period 2020-2024, a 40 percent reduction. This recalibration in new supply is expected to persist until 2030.

Also, policy interest rate settling to 4.5 percent to 5 percent by end 2025 will positively impact the recovery efforts of the office space industry.

Lobien continued to say that the BPO industry ended strongly in 2024, garnering USD 38 billion worth of revenues and reaching a total of 1.82 million workforce headcount. By end of 2025, the sector expects to generate USD 40 billion and gain an additional 80,000 labor force, which translates to the need of 300,000 – 400,000 square meters (sqm) of office space in the country, primarily in the central business districts (CBDs). The 1.82 million FTEs as of end 2024 puts the 2.5 million FTE goal of the IT-BPM industry by end of 2028 within reach, which translates to an additional office requirement of around three million sqm over four years.

Demand for office space will remain strong from the BPO industry in 2025. After traditional offices, which take up 44 percent of total office space demand, companies under the IT-BPM industry come in at 35 percent by Q2 2025. Interestingly, government agencies have also taken their share of office space demand at 15 percent, which positively contributed to the recovery of the office market in the first half of 2025.

Co-working setups or flexible office remain an alternative office space strategy for companies which are not ready to invest in leasing traditional office spaces. This is favorable for firms that need physical office space not exceeding 100 sqm and where rental is on a per seat leasing basis and can be increased or decreased more flexibly than a traditional office. As of 2025, there are around 210 co-working spaces within Metro Manila occupying around 300,000 sqm of office space.

Lobien ended her presentation by saying that the office sector will remain a “tenant’s market” in 2025. Hence, companies and businesses with plans for expansion or relocation should take this opportunity to browse through the market and invest in the right office location that fits their requirements. Overall, investors can collaborate with landlords and negotiate office rental at rates even lower than the ongoing average rental rate.

NCR residential market

According to the Bangko Sentral ng Pilipinas (BSP), the total real estate prices for various types of new housing units in the Philippines increased 7.6 percent y-o-y in Q1 2025. Lobien said during her presentation for the residential market that the National Capital Region (NCR)’ housing prices increased by 13.9 percent while residential property prices in the provincial areas contracted by 3 percent. Per housing type, condominium prices rose 10.6 percent.

In terms of residential real estate loans granted, NCR had 27.4 percent while CALABARZON had 29.9 percent, followed by Central Luzon at 13.8 percent. By type of housing unit, six of every ten (60%) residential real estate loans were for houses, while four of ten (40%) loans were for condominium units. The BSP report on loans granted and concentration is in accord with 2021 DHSUD (Department of Human Settlements and Urban Development) which shows that there are 1.4 million housing requirements in CALABARZON and 697,000 units in NCR.

Lobien said that the current over-supply in the condominium market points to a “buyer’s market” in the residential sector and the prevailing offers of better prices, higher discount rates and longer payment options for the downpayments from developers are good inputs to residential buyers and investors.

The provincial office market

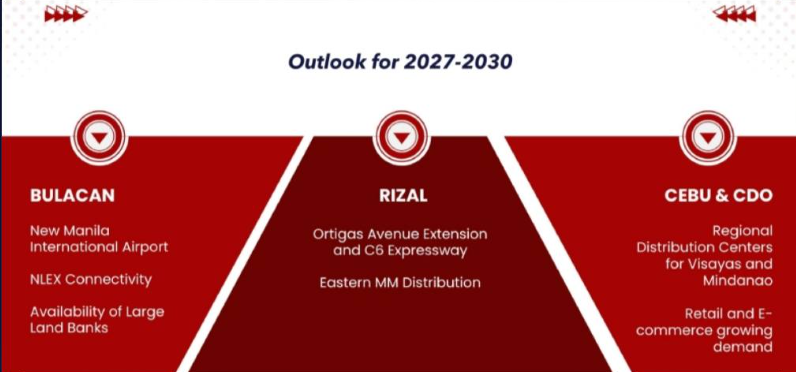

LRG COO Jericho Linao gave the following analysis of the provincial office market. As of 2Q 2025, the vacancy rate of the office market in the provincial areas is still elevated at 30 percent while lease rate remains at 7 percent. The high vacancy rate in NCR also gives incentive to locators to exhaust available spaces in the NCR before moving to the provinces. Nevertheless, infrastructure projects of the government like the highly anticipated ‘Luzon Spine Expressway Network’ (along with other transportation developments that supplement it) should soon be expected to help drive demand to provincial areas. With this, major real estate developers are on the right track of establishing townships outside the NCR to supplement office space demand, with concentration in Pampanga, Cavite, Laguna, and Rizal.

Linao added that the average office market rental rates in the provinces marginally increased to Php 565.00/sqm for 2Q 2025 versus last year’s Php 550.00/sqm. This minimal rise increase can be attributed to the rise of rental rates of strong provincial locations with improving office markets like Cebu (from Php 570.00/sqm to Php 635.00/sqm), Iloilo (from Php 585.00/sqm to Php 610.00/sqm), and Cavite (from Php 500.00/sqm to Php 600.00/sqm).

Industrial market

Meanwhile, according to LRG Associate Director Steph Ng, In the industrial real estate sector, the market size of Philippine warehousing is expected to reach USD 447 million by year end 2025 at a compound annual growth rate (CAGR) of 54.2 percent. The market size is expected to reach USD 680 million by year 2033. The country’s warehousing market is primarily driven by the companies in the manufacturing, logistics, and E-commerce industries.

As of Q2 2025, majority of the warehouse supply can be found outside NCR, particularly in the nearby provincial areas. CALABARZON remains a top location for industrial real estate, but the supply extends even further to Pangasinan in the North. Outside Luzon, warehouse supply is also strong in Cebu, Davao, and Cagayan De Oro. Real estate developers, like RLX, has continuously expanded its warehousing footprint nationwide.

Real estate industry conclusion

The LRG team’s interaction with the media during the last part of the presentation also led to the following conclusions. Although the Philippines has been resilient economically and has been registering high GDP growth as compared to peers, the recovery in the office sector is slower-than-expected due to the natural lag in office market recovery, global growth slowdown (from 3.3 percent in 2024 to 3 percent in 2025), and the lingering effect of the POGO exit. These are on top of the high inflationary environment and higher-for-longer policy interest rates that persisted in the country in 2023 and 2024, geopolitical tensions like the Ukraine-Russia war and the conflicts in the Middle East, and uncertainties caused by the reciprocal tariffs being initiated by the United States.

With respect to the best time to engage in the residential and office space markets, knowledge of the real estate cycle is a good guide. The expected additional reductions in policy interest rate for the rest of the year will help in making the right timing for this decision for residential buyers and investors, as well as by office locators. However, decrease in vacancy rates and supply will impact the negotiating leverage of buyers or locators.

Finally, another investment avenue in the real estate industry is the REIT (Real Estate Investment Trust) where estimated dividend yields range from 6.1 percent to 9.2 percent, which addresses any liquidity requirement of investors while stock price appreciation will be for the longer term pay-off from this type of investment.

Read article: https://www.manilatimes.net/2025/07/15/business/real-estate-and-property/lobiens-2025-mid-year-report-of-the-real-estate-industry/2149397